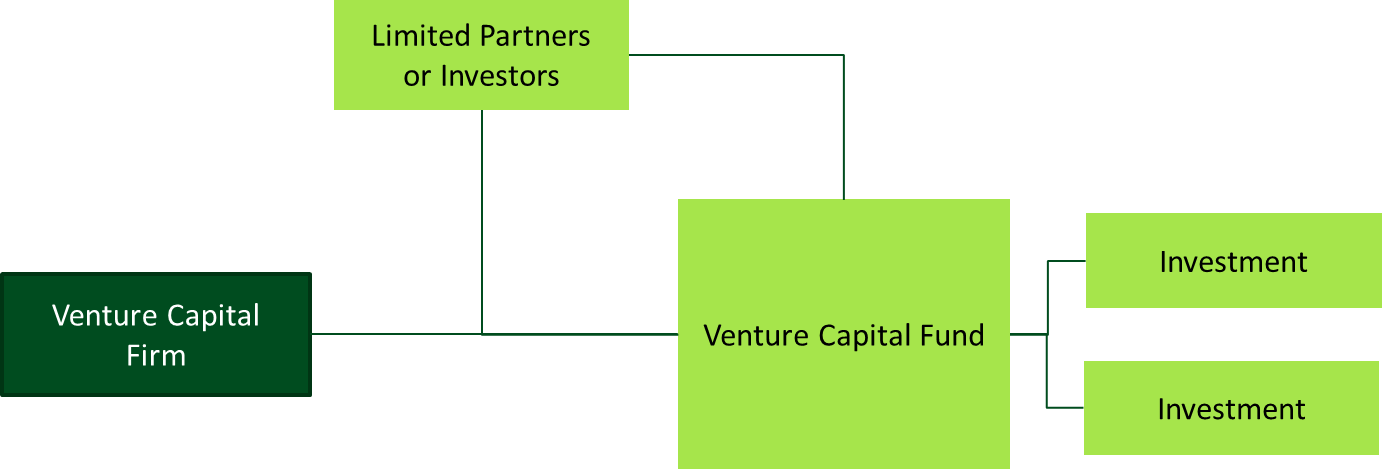

Venture capital firms are typically structured as limited partnerships. The VC firm is the general partner, but there can also be more than one. A general partner takes an active role in managing the businesses in the fund. They have extensive business experience at the executive level. Working at a VC firm means you will be supporting the general partners.

Investors are limited partners. They can be high net worth individuals or financial institutions like insurance companies, banks, and pension funds. Limited partners are not involved with the daily operations of the firm. You won’t see their representatives walking around the office every day. They are passive capital providers.

Has the VC structure broken down? That is the question that some people are asking after Adeo Ressi, founder of TheFunded.com, made a presentation that criticized the industry. He argues that VC firms have become money magnets that attract capital but fail to produce positive returns. They have transformed into ineffective bloated capital structures that drag down the economy.

Ressi says there is too much money chasing too few deals. This has boosted valuations to unsustainable and unprofitable levels. Larger companies like Yahoo, Microsoft, Google, and Cisco have wised up to the VC game. Rather than face the prospect of a large formidable competitor in the future, they often resort to buying companies with any sign of potential to ward off threats.

Skype is one example of what happens when you don’t buy quickly enough. Ebay bought Skype in 2005 for $2.5 billion. In 2009, Silver Lake and Andreessen Horowitz bought a 65% stake in Skype with a valuation of $2.75 billion. In 2011, Skype changed hands again when Microsoft bought them for $8.5 billion. If you don’t buy it early, it will just get flipped back to you.

If VC firms don’t generate significant returns, they face the risk of becoming asset gatherers who merely extract fees for no additional value added. VC firms can make money even if their limited partners lose. Like hedge funds, venture capitalists charge a 2% management fee. In most VC funds, the partners’ capital accounts for just 1% of the total assets. So in 6 months, their accrued management fees have already covered their risk. Everything else after that is gross profit. That’s the kind of risk/reward situation a venture capitalist loves.